Keynesian Economics and Monetary Disequilibrium

What is Keynesian Economics about? Even if you've never taken an economics class you might still have some idea. The 2008 stimulus package was frequently referred to as a Keynesian policy. Government intervention and Keynesian economics often go hand and hand. If you have taken a macroeconomics class you might have an even deeper knowledge of Keynesian economics. Maybe you know about the multiplier, the Keynesian cross, the IS-LM model. And all of those are certainly related to Keynesian economics, but none really capture the heart of Keynes's contribution.

Part of the trouble with people's understanding of Keynes's work is that secondary sources frequently distort what he actually said. For example, if you read Mankiw's intermediate macroeconomics textbook you will come away with the impression that Keynesian economics is about sticky prices. We get unemployment because wages don't adjust downward quickly enough. So called "New Keynesian" models, the modern analogue to IS-LM are also predicated on slower than optimal price adjustments to shocks. It is true that Keynes assumed sticky prices for part of his analysis, but he was careful to emphasize that "The essential character of the argument is precisely the same whether or not money-wages, etc., are liable to change" (General Theory Ch. 3).

So if not sticky prices or wages, what is it that causes unemployment in Keynes's world? In my reading, Keynes's story is all about monetary disequilibrium and a failure to coordinate savings and investment in a monetary economy.

Keynes famously stated that his theory refuted "Say's Law," which can be simply stated as "supply creates its own demand." Now, whether or not that's what Say actually said remains a point of contention even today, but it's that formulation that Keynes attempts to refute, which I think is worth exploring on it's own. What Keynes really wants to do is draw a distinction between a barter economy and a monetary economy. I recently taught an intermediate economics class and I developed a simple example that I think helps illustrate the main points.

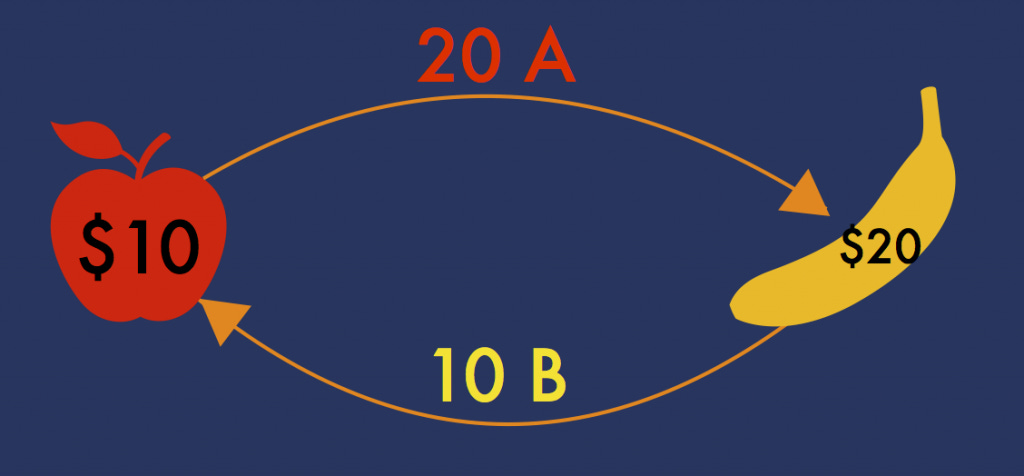

Let's start with an economy with no money and only two goods, apples and bananas. There are two people in the economy. Person A can only produce apples and person B can only produce bananas. For simplicity, I will assume a fixed price ratio of 2:1. One banana is worth as much as two apples. The story gets more complicated if we allow this price to change, but I don't think the main implications would be any different. In this economy with no money, the only trade that can occur is bananas for apples. If A wants to demand 10 bananas from B, he needs to produce 20 apples. It is in this sense that supply creates its own demand. Without money, demand for one good is precisely supply of another. The diagram below illustrates what is happening (I arbitrarily fixed prices in dollar terms, but remember there is still no money. Dollars operate only as a unit of account)

In this kind of barter setup, Say's law is trivially true. Any demand for bananas is supply of apples so supply creates its own demand. In this case, demand for bananas is $10(20) = 200 and supply is $20(10), which are obviously equal. However, when we start to add in money, the relationship between supply and demand is not as clear.

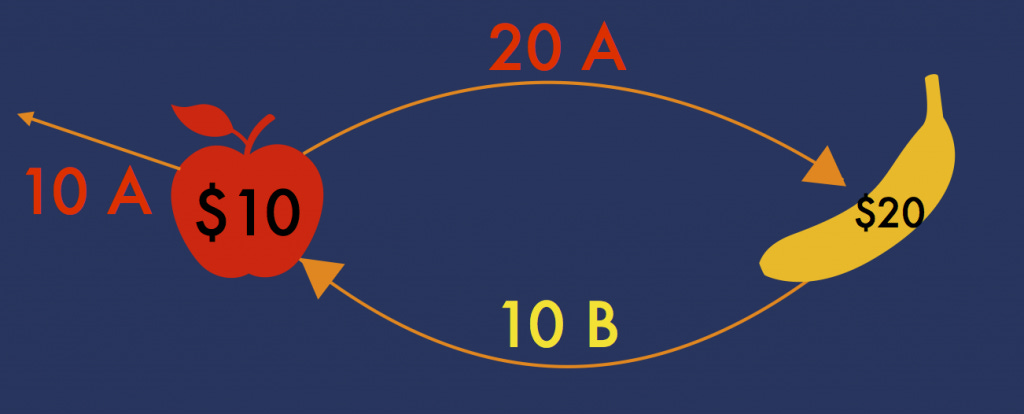

For a second example we will assume now that bananas and apples cannot be directly traded. Instead, each good will have to be sold for dollars, which can then be used to purchase the other good. Of course, we could still have the exact same situation as above. If all transactions happen instantaneously and every time an apple is produced it is immediately sold and the proceeds immediately used to purchase an apple. However, now there is another possibility.

Imagine that for some reason the apple producer wants to consume more bananas tomorrow than today and decides to save in dollars (I assume apples cannot be saved directly - this might be a strong assumption but it will make sense later). He still wants to consume 10 bananas (so he needs to produce 20 apples), but he also wants to save $100, so he produces an additional 10 apples (30 apples total). But what if the banana producer still only wants to buy 20 apples. He doesn't want to pay an extra $100 for the additional 10 apples that are being produced.

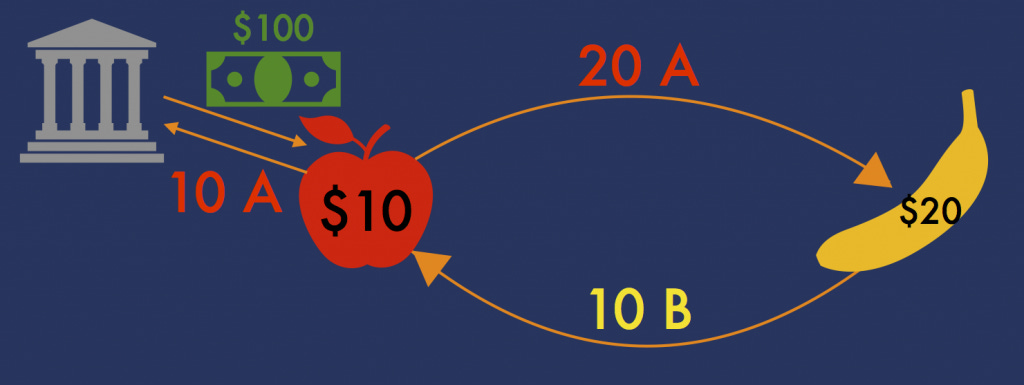

If you're an economist the first question that comes to your mind should be why the price doesn't just adjust. If demand for apples is less than supply for apples, the price of apples should fall until the market is equilibrated. So in this case, apples could fall in price to $6.67 so that 10 bananas buy 30 apples and supply equals demand again. Except then we run into a problem. After the price adjustment producer A still isn't happy. He didn't get to save his $100. So really this can't be an equilibrium at all (it's possible that the change in prices would also affect his desired saving, but as long as it's still positive it's still not an equilibrium).

The problem with the logic above is that we are still trying to think of the economy as a barter economy with one market (trade between apples and bananas), when it is actually a monetary economy with 2 markets (money for apples and money for bananas). Finding a single equilibrium price for two markets is not enough. We need equilibrium in both markets. What we have in the example above is an excess supply of apples and an excess demand for money. The banana producer can't supply additional money, so he is unable to help return to equilibrium. So who can help? Who supplies money? The Fed! If the Fed simply prints money to buy the excess apples we are back to equilibrium at the same prices as before.

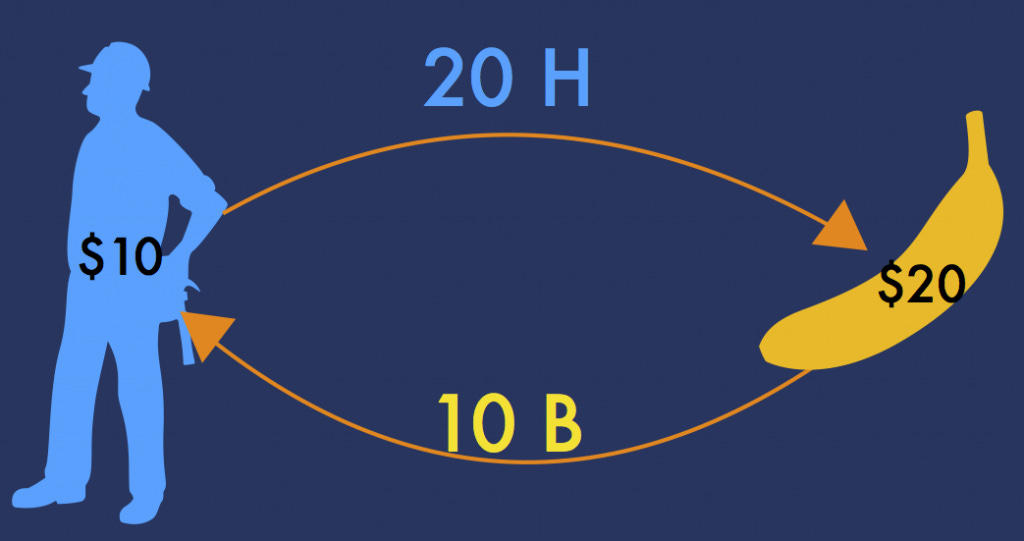

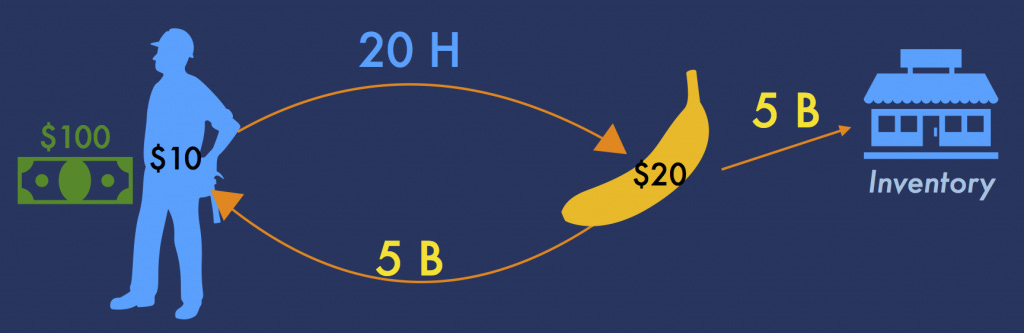

So what does any of this have to do with unemployment? Let's change the example slightly. Instead of apples, assume now that A provides labor. They work for B to produce bananas. If this is a barter economy then their wage is paid in bananas (I still fix arbitrary dollar values) and demand and supply are always equal as above:

But what if the worker wants to save? He obviously can't save labor directly (which is why I assumed no saving of apples above) and I will assume he doesn't have the storage to save bananas either. Instead, he will try to save in dollars by buying fewer bananas (but working the same amount). If he wants to save $100 the picture becomes:

Since the worker still worked 20 hours, production of bananas didn't fall, but demand for bananas did. The firm is forced to put the extra bananas into its inventories. Is this a problem? Maybe not. If the firm realizes that the worker will use his savings to purchase more bananas in the future, they are happy to increase their investment now in order to produce more bananas next period (an equivalent story could be told where they are building machines to increase production, but the inventory version is the simplest I think). We could then imagine a second period of this economy where the worker uses his savings from the first period to buy the bananas from the inventory in the second.

This story gives us a nice equilibrium outcome with no unemployment. The worker works his desired amount in each period, saving $100 in the first to buy five additional bananas in the second. The banana producer invests in 5 extra bananas to prepare for the increase in demand in the second period. Saving and investment are perfectly coordinated. Say's Law holds.

But it is easy to imagine another equilibrium. What if the firm does not realize demand for its product will increase next period? All it knows is that consumers want to buy 5 fewer bananas right now. In this simple example where there is only one option for the worker to spend his money that's hard to believe, but in the real economy with thousands of firms and millions of products, an individual producer has no idea whether increased savings will translate to future demand for its own product. If demand falls today, they might predict lower demand tomorrow as well. In this case they will not want to increase investment today. Instead they simply cut production. So we have a worse equilibrium that looks like

Here the firm doesn't expect the decline in demand today to translate into an increase in demand tomorrow. They see demand for 5 bananas today so they only hire the worker for long enough to produce those 5. The worker still wants to work 20 hours to save an additional $100, but nobody will hire him so he only works 10 and is therefore underemployed (if we think about this as representing many people we would have some employed and some unemployed). Keynes referred to this situation as involuntary unemployment. People want to work at the prevailing wage, but since firms don't expect their consumption of their product to compensate the cost of their wages, they don't want to hire.

There are two interesting points here. First, note that wage cuts will not help. The worker wants to save regardless of his wage. Cutting it will only make him want to work more, which actually makes the problem even worse. Second, the firm's prediction actually comes true. Since the worker was actually unable to save anything in the first period, his demand for bananas actually won't increase in the future either. By expecting lower demand tomorrow, the firm actually caused that future to be realized. In this way, expectations are self-fulfilling and we get multiple equilibria.

This example is highly stylized, but I think it demonstrates Keynes's main point. When somebody wants to save, there is no magical process that instantly transforms their saving into investment. Investment decisions are driven primarily by firms' expectations about demand for their own products. Without perfect foresight, they must rely on cruder measures of prediction (like animal spirits). If they don't expect increased saving to translate into future demand, we get unemployment.

I will have more to say on Keynesian economics in at least one future post (including some criticism of Keynes), but this is already getting long so I will stop here for now.